Out-of-Pocket Maximum: What It Means and How It Affects Your Health Costs

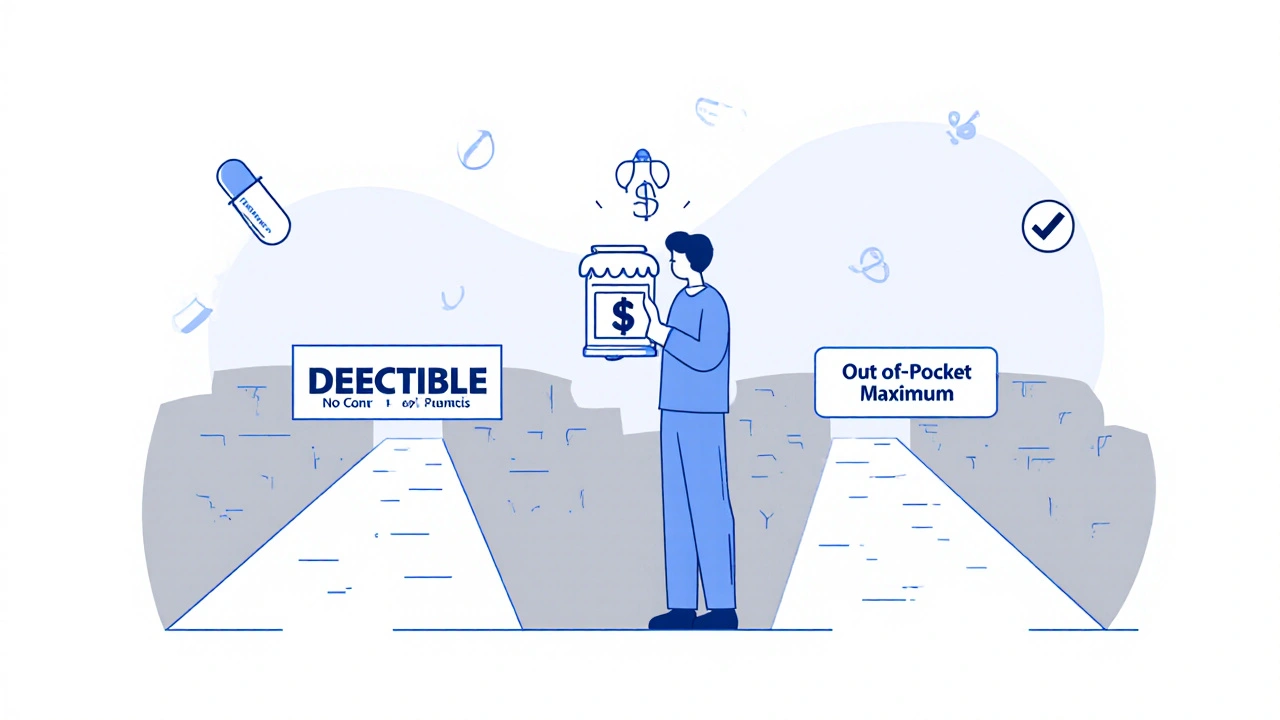

When you hear out-of-pocket maximum, the total amount you pay for covered healthcare services in a plan year before your insurance pays 100%. Also known as annual out-of-pocket limit, it’s the safety net that stops your bills from climbing forever—even if you need surgery, chemo, or a long hospital stay. This number isn’t just a line on a form. It’s the line between financial stress and peace of mind.

Think of it like this: you pay a deductible, the amount you pay before insurance starts sharing costs first. Then you pay copays and fixed fees for doctor visits or prescriptions and coinsurance, which is a percentage of the cost. All those payments—except your monthly premium—add up toward your out-of-pocket maximum. Once you hit that number, your insurance picks up 100% of covered services for the rest of the year. No more bills for that plan year. No surprises. Just care.

Here’s what most people don’t realize: your out-of-pocket maximum doesn’t include your premium. It also doesn’t cover services your plan doesn’t cover at all—like cosmetic procedures or out-of-network care unless it’s an emergency. And if you’re on a high-deductible plan, you might hit that maximum faster than you think, especially if you’re managing a chronic condition like diabetes or gout, or need ongoing treatments like antivirals for hepatitis C or joint protection for gout. The same goes for seniors on diabetes meds or people on long-term hormone therapies like exemestane—those monthly costs add up fast.

Knowing your out-of-pocket maximum helps you plan. If you’re starting a new medication like pirfenidone for lung fibrosis or esketamine for depression, you can ask your provider: "Will this be covered? What’s my coinsurance?" That way, you won’t get blindsided by a $1,200 prescription bill. You can compare plans not just by monthly cost, but by how high the maximum is. A plan with a $3,000 out-of-pocket maximum might be better than one with a $1,500 deductible if you need frequent care.

It’s not just about drugs. It’s about ER visits, lab tests, physical therapy, even telehealth visits. If you’ve ever had a CT scan with contrast, or needed premedication with steroids before a procedure, you’ve paid toward that limit. If you’ve been on gabapentin with opioids, or switched from methadone to buprenorphine, you’ve seen how medication choices affect your wallet. Your out-of-pocket maximum ties all of it together.

Check your plan documents every year. Don’t assume it stays the same. Employers change plans. Insurance companies adjust limits. The out-of-pocket maximum for 2024 might be higher than last year’s. And if you’re on Medicare or a supplemental plan, know how it stacks up with your primary coverage. You don’t want to pay twice for the same service because you didn’t understand the rules.

Below, you’ll find real stories and practical guides from people who’ve been there—how to avoid overdose when restarting meds, how to manage side effects from cancer drugs, how to spot fake pills, and how to use shared decision-making to pick treatments that fit your budget and your life. This isn’t theory. It’s what happens when you know what you’re paying for—and when you finally get to stop paying at all.