Most people think if they’re paying for prescriptions, those payments should chip away at their deductible. But that’s not always true. And if you don’t understand how generic copays work with your out-of-pocket maximum, you could be paying way more than you need to - even after you think you’ve met your deductible.

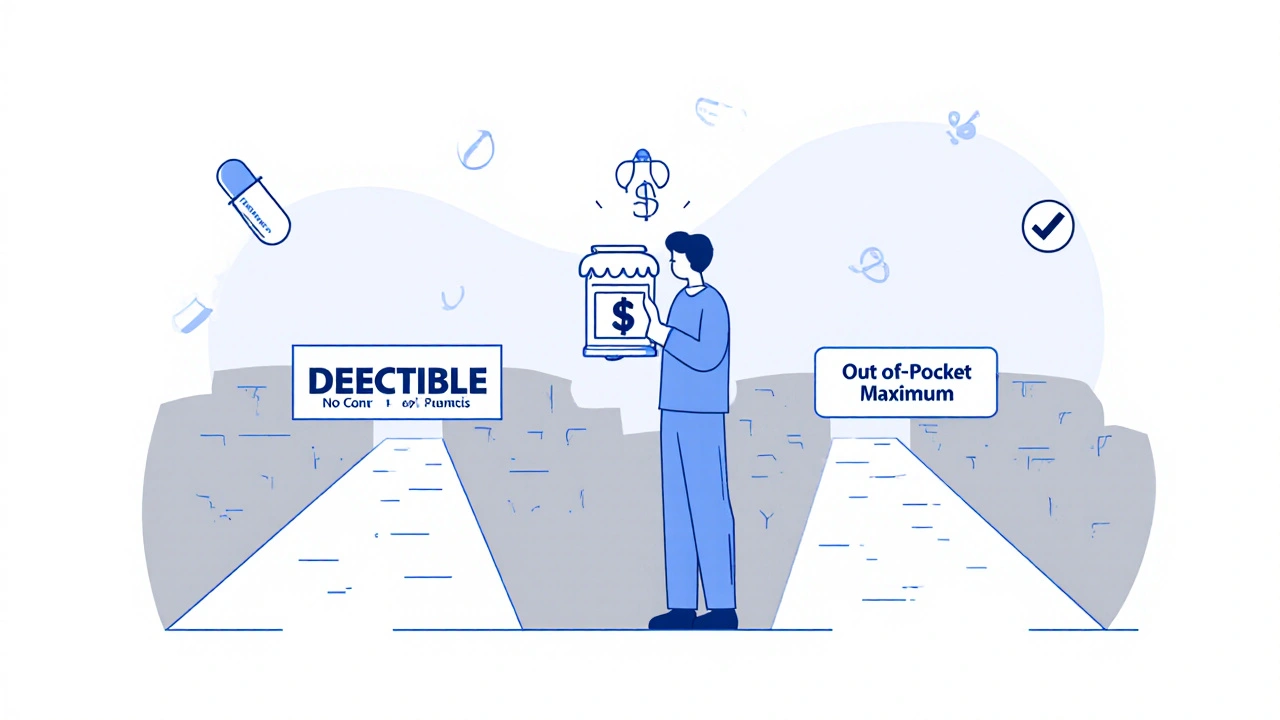

What’s the difference between a deductible and an out-of-pocket maximum?

Your deductible is the amount you pay before your insurance starts sharing the cost of covered services. For example, if your deductible is $2,000, you pay 100% of eligible medical and prescription costs until you’ve spent that much in a year.

Your out-of-pocket maximum is the most you’ll pay in a year for covered care. Once you hit that limit, your insurance pays 100% of everything else for the rest of the year. For 2025, the federal cap is $9,200 for an individual and $18,400 for a family on Marketplace plans.

Here’s the key: all your in-network cost-sharing - including deductibles, coinsurance, and copays - counts toward your out-of-pocket maximum. But only some of it counts toward your deductible.

Generic copays don’t usually count toward your deductible

Let’s say your plan has a $1,500 medical deductible and a $10 copay for generic prescriptions. You fill your blood pressure med every month. That’s $120 in copays by the end of the year. You might assume that $120 reduces your deductible. It doesn’t.

Those $10 payments go straight to your out-of-pocket maximum - not your deductible. So even if you’ve paid $2,500 in copays over the year, your deductible is still $1,500. You haven’t met it. You still pay full price for doctor visits or lab tests until you hit that $1,500 mark.

This setup was created by the Affordable Care Act in 2014. Before then, copays didn’t count toward anything. You paid them, and they vanished. The ACA fixed that by making sure copays count toward your out-of-pocket maximum. That’s a big win if you have chronic conditions - but it also created confusion.

Why does this matter?

Imagine you’re managing diabetes. You pay $15 copays for insulin every month. That’s $180 a year. You think you’re getting closer to meeting your $3,000 deductible. But you’re not. You’re only getting closer to your out-of-pocket maximum.

That distinction changes everything. Once you hit your out-of-pocket maximum - say $6,000 - your insulin becomes free for the rest of the year. But your next doctor visit? Still full price until you hit your $3,000 deductible.

A 2023 survey by America’s Health Insurance Plans found that 68% of people think prescription copays count toward their deductible. Only 22% got it right. That misunderstanding leads people to skip meds they can’t afford - or keep paying for services they think are covered.

Three plan types you might have

Not all plans are built the same. There are three common structures:

- Single deductible - One amount covers both medical and prescriptions. If you pay $10 for a generic drug, it counts toward that single deductible. This is the simplest, but only 27% of employer plans use it.

- Separate deductibles - You have a medical deductible (say $2,000) and a prescription deductible (say $500). You pay full price for meds until you hit the prescription deductible. After that, you pay copays. Those copays count toward your out-of-pocket maximum, but not your medical deductible. This is the most common - used in 37% of plans.

- Copay-only with no prescription deductible - You pay your $10 copay right away, no deductible to meet. But again, those $10 payments don’t reduce your medical deductible. They only help you reach your out-of-pocket maximum. Used in 36% of plans.

If you’re not sure which one you have, check your plan’s Summary of Benefits and Coverage (SBC). Look for the section that says: “Does this payment count toward my deductible?” If it says “No” for copays, you’re in one of the two models where copays don’t help your deductible.

What you should do right now

Don’t guess. Don’t assume. Open your plan documents - the SBC and the Explanation of Coverage. Find these three things:

- What’s your medical deductible?

- Is there a separate prescription deductible?

- Do copays count toward your deductible? (Look for a yes/no column.)

Most plans are required to give you this info before you enroll. If you don’t have it, call your insurer. Ask: “Do my generic prescription copays count toward my medical deductible?”

If the answer is no - and you’re paying $200+ a year in copays - you’re not getting closer to meeting your deductible. But you are getting closer to hitting your out-of-pocket maximum. That’s still good. Just know which one you’re chasing.

Real stories from real people

On HealthCare.gov, a user named “MedicareMom” wrote: “I paid $10 copays for my blood pressure med all year. I thought I’d met my $2,000 deductible. Turns out I hadn’t. I still paid $1,200 for a specialist visit.”

On Reddit, someone said: “I thought my $15 insulin copays were reducing my deductible. I was shocked when my plan said I still owed $1,800 to meet it. I paid $1,800 in copays - and it didn’t count.”

But not all stories are bad. “DiabetesWarrior” on PatientsLikeMe shared: “Before 2014, my copays didn’t count for anything. Now, they count toward my $8,500 out-of-pocket max. Last year, I hit it in October. My insulin was free for the rest of the year. That saved me $3,000.”

The future is changing - slowly

The government knows this system is confusing. In April 2024, the Department of Health and Human Services announced new rules for 2025 plans: insurers must make it clearer how copays count.

Some insurers are testing “Integrated Deductible” plans - where prescription costs, including copays, count toward one single deductible. Early results show patients take their meds more consistently.

McKinsey predicts that by 2027, 60% of major insurers will offer at least one plan where generic copays count toward the deductible. But the American Hospital Association warns that simplifying this could raise premiums by 3-5%. So it’s a trade-off: simpler rules, or lower monthly costs?

For now, the system stays complicated. But you don’t have to be confused by it.

Melania Rubio Moreno

i thot copays counted toward deducible lol. guess i been payin for nothin but my meds are free now so i aint mad. #healthcareconfusion

Gaurav Sharma

This is a fundamental failure of the American healthcare architecture. The bifurcation of deductible and out-of-pocket maximum is not merely confusing-it is predatory. Patients are deliberately obfuscated into financial vulnerability.

Shubham Semwal

yo so i been payin $15 for insulin every month and thought i was gettin closer to meetin my $3k ded? nope. just got closer to my $8k OOP max. my doc visit last month still cost me $900. this system is designed to make you feel like you're winnin while you're gettin robbed.

Sam HardcastleJIV

The structural complexity of health insurance in the United States reflects a broader societal failure to prioritize clarity and equity in essential services. One must question the ethical implications of such obfuscation.

Mira Adam

You people are still surprised by this? Of course they don't count. The whole point is to keep you paying. Insurance companies don't want you to hit your max-they want you to stay broke and dependent. This isn't a bug. It's a feature.

Miriam Lohrum

It's interesting how the ACA tried to fix one problem but created another layer of misunderstanding. People think they're making progress when they're just moving money between different buckets. Maybe we need a simpler metaphor-like a bank account with two separate vaults.

archana das

In India, we don't have this mess. You pay monthly premium, then you pay doctor fee or medicine cost-no hidden rules. But here, it feels like a game where the rules change every time you blink. Why make life harder?

Emma Dovener

I used to work in benefits administration. Most people don’t even know what an SBC is. If you don’t check it, you’re flying blind. I always told clients: print the SBC, highlight the yes/no column for copays, and tape it to your fridge. Seriously.

Sue Haskett

I just want to say-PLEASE, please, please-open your plan documents. Seriously. Look at the Summary of Benefits and Coverage. It’s not that hard. It’s literally one page. If you don’t know whether your copays count toward your deductible, you’re playing Russian roulette with your health money. I’m not being dramatic-I’m being a friend.

Jauregui Goudy

I hit my out-of-pocket max in July last year. My insulin? Free. My MRI? Free. My follow-up? Free. But my doctor visit in March? Still $400. That’s the trap. You think you’re done paying-but you’re only done paying for the stuff that counts toward the max. The deductible? Still waiting. This system is a psychological rollercoaster.

Tom Shepherd

i just checked my plan and turns out my copays dont count toward ded but do count toward oop max. i had no idea. now i know why i still owe $1200 for my specialist. this is wild. thanks for the post.